The Seeking Alpha transcription team is responsible for the development of all our transcription related projects. We currently publish thousands of quarterly earnings calls quarter after quarter on our site and continue to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new developments related to transcripts. Thanks, SA Transcripts Team

The Seeking Alpha transcription team is responsible for the development of all our transcription related projects. We currently publish thousands of quarterly earnings calls quarter after quarter on our site and continue to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new developments related to transcripts. Thanks, SA Transcripts Team

I have always been attracted to companies that have interesting business models. The more traditionally “boring” the companies in question are, the more excited I tend to be about them. It’s one company she caught my attention in October the year was 2022 Strattec Security Corporation (NASDAQ:STRT), a company that focuses on the production and sale of locks and keys for its customers. These include mechanical locks and keys, but also electronically enhanced ones. The company also manufactures dashboard ignition lock covers, latches, power sliding side door systems, power tailgate systems and more.

In October 2022, I found myself interested in the business. Although the company was small and fundamentally volatile, the stock looked attractive. At the time, the company was dealing with the pain of a shortage of semiconductors. But because of how cheap the shares were, I felt rewarded justified the risk. This led me to rate the trade a “buy” to reflect my view at the time that the stock should outperform the broader market for the foreseeable future. Fast forward to today and the company has been doing well, delivering a 24% return to investors. But unfortunately, this growth fell short of the 37.7% increase seen by the broader market over the same time period. If future estimates turn out to be accurate, the company is not looking bad at all. But between the rising share price and the high level of volatility that shareholders face, I’d argue that there are better opportunities out there right now.

Look elsewhere

Basically, the picture for Strattec Security has been pretty shaky since I last wrote about the business. Consider e.g. Result for first half fiscal year 2024. According to management, sales this time amounted to $253.9 million. That’s up 8.7% from the $233.5 million generated a year earlier. Management attributed this increase primarily to the higher prices it charged its customers. This helped bring in $18.8 million in sales. The end result was a $15.5 million margin improvement.

By SEC EDGAR Data

From a profit perspective, the bottom line was a nice increase in net income from a negative $1.7 million to a positive $5.2 million. While the company saw some margin improvement from a sales perspective, there were some areas of weakness. For example, the business had to contend with $2.3 million in increased shipping costs. Wages and benefits increases in Mexico also hit the company $2.8 million. And sales were negatively impacted by $5.8 million due to foreign currency fluctuations. Despite all these pains, most of the company’s profitability indicators improved year-on-year. Yes, operating cash flow actually increased from $8.7 million to negative $6.9 million. But if we adjust for changes in working capital, it rose from $6.6 million to $14 million. Meanwhile, EBITDA for the business rose from $3.7 million to $14.7 million.

By SEC EDGAR Data

As for the second quarter of fiscal 2024 itself, we see a similar situation. Revenue of $118.5 million was up 4.7% from the $113.2 million reported a year earlier. The firm went from generating a net loss of $1.8 million to a profit of $1 million. Other profitability metrics followed as well. The only exception was operating cash flow. It fell from $4 million to negative $3.9 million. But on an adjusted basis, it more than doubled from $2 million to $4.6 million. Finally, EBITDA for the company fell from a negative $0.5 million to a positive $4.3 million.

In terms of pricing, the stock looks fairly cheap based on the future. Unfortunately, because management does not provide detailed year-to-date guidance and due to volatility, there is significant uncertainty in these estimates. If we simply annualized the results for the first half of the year, we would have expected adjusted operating cash flow of $14.2 million and EBITDA of $42.5 million. However, since there has historically been at least some relationship between adjusted operating cash flow and EBITDA, I decided to use a more conservative estimate for EBITDA of $14.9 million.

By SEC EDGAR Data

Using these estimates, I was able to value the business as shown in the chart above. Based on 2023 estimates, the stock looks decent, but not incredibly cheap. But based on the front they look quite attractive. I then compared the company to five similar firms as shown in the table below. According to 2023 estimates, four out of five businesses were cheaper than others on a price-to-operating cash flow basis. And when it comes to EV’s approach to EBITDA, that number drops to three.

Clearly, Strattec Security is not the cheapest opportunity. However, it is worth noting that if we were to use forward estimates, his ranking with the EV-to-EBITDA approach remains unchanged, while with the price-to-operating cash flow approach, we find that two out of five are cheaper than him.

From a pricing perspective, it’s clear that there are other opportunities in the space that could be worth considering. Furthermore, while the stock is attractive on a forward basis, it’s not like it’s in a bargain. That doesn’t mean the company isn’t worth paying attention to. While I am personally downgrading from “buy” to “hold” due to the factors mentioned above, there are reasons for optimism in the long term. For beginners, vehicle sales are on the rise again. After falling to 13.9 million domestically in 2022, new car sales increased to 15.5 million in 2023. And this year, a further drop to 15.7 million is expected. Unfortunately, this is still below the 17.5 million that was the all-time high in 2016. But the trend is clear.

Strattec Security

Some investors may point to the fact that the vehicle market is international. It is true. Unfortunately, Strattec Security Corporation management did not disclose the geographic breakdown of the company’s revenue. But we do know that roughly two-thirds of the company’s sales come from the traditional Big Three automakers. General Motors Company (GM) gets about 81.2% of its revenues from USA Ford Motor Company (F) generates about 75.6% of its revenue from North America as a whole. AND Stellantis NV (STLA) generates about 48.6% of its revenue from North America. So it’s safe to say that what’s happening in the US market plays a huge role in the overall health of our candidate. So with vehicle sales growing here at home, the company should be doing quite well.

Take away

From everything I can see, Strattec Security Corporation remains a very interesting business. However, it is not a great business. Volatility is problematic and stocks have risen quite a bit. The stock isn’t expensive by any means, but it’s no longer incredibly cheap like it used to be. All this convinced me to downgrade the company.

But that doesn’t mean I think the future of Strattec’s business will be bad. In the long term, sales and profits are likely to continue to grow. But I just don’t think the picture will be compelling enough to justify a rally in the markets.

Editor’s note: This article covers one or more microdroplet stocks. Please be aware of the risks associated with these shares.

The Seeking Alpha transcription team is responsible for the development of all our transcription related projects. We currently publish thousands of quarterly earnings calls quarter after quarter on our site and continue to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new developments related to transcripts. Thanks, SA Transcripts Team

Tecnoglass Inc. (NYSE:TGLS) with roots in Colombia (although 96% of its revenue comes from the US) is a vertically integrated provider of building products for the commercial and residential construction industry. TGLS is known primarily for its expertise in the field of architectural glass and windows, although it also provides aluminum products such as profiles, bars, plates, rods, etc.

Over the past year, TGLS has proven to be a highly rewarding offering, delivering ~35% total returns, more than 2x its industry peers and more than 1.6x its benchmark index.

YCharts

If one digs deeper, it’s not hard to see why the market likes this business.

Tecnoglass – What is good

The vertically integrated Tecnoglass lineup is a great asset in a space that is inherently quite commoditized, with limited points of differentiation. By vertically integrating some key functions such as sourcing, manufacturing, distribution, etc. the company can gain better efficiency which ultimately translates into better margins. Notice how EBITDA margins, which were only around the 10% mark, have increased almost 4x and are currently approaching the 38% mark.

YCharts

In terms of resources, its minority stake in Saint-Gobain’s Float Glass Operation in Colombia ensures a steady and reliable source of glass supply, mitigating the risks of constant price fluctuations.

Then, even though the vast majority of its business takes place in the US, TGLS is in a pretty good position on the manufacturing cost front because the manufacturing is done in Colombia. TGLS’s job offer is compelling enough in that it offers a 15% premium over Colombia’s minimum wage rates, but the discount to US manufacturing wages is still quite meaningful, so their total labor costs are also quite competitive. – with other North American peers.

Also in terms of transport, it is fair to say that the demand for high-end architectural glass originates mainly from coastal cities and therefore it would make more economic sense to ship it rather than resorting to ground transport, which can be more cumbersome and expensive. . In this regard, the flagship TGLS production unit in Barranquilla offers quite an advantage as it is strategically well located near three key ports – Barranquilla, Cartagena and Santa Marta.

All of these factors will play out to give TGLS a competitive fixed cost base, and then when the business momentum is resilient enough, you’ll start to see strong operating leverage.

Speaking of business momentum, note that the company’s order backlog (primarily commercial and multifamily) is currently growing at a rate of 20% and recently reached 836 million dollars. This build-up typically takes 12-18 months to realize, so one has a decent view of sales through FY25 even if the market takes a turn for the worse.

Now for the 836 million backlog, you also have a wildcard in the form of single-family residential products, which typically have much shorter lead times. Management highlighted how they have seen increased traction and a wider dealer base here as the market recognizes TGLS’ ability to deliver product in as little as 5-6 weeks.

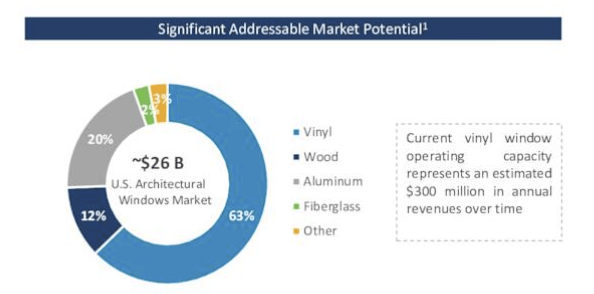

TGLS’s investment case is further bolstered by the fact that it also entered the lucrative vinyl window glass market in the third quarter of last year (growing demand for energy-efficient products should benefit this product), which accounts for a whopping 63% of the total architectural window market . This essentially doubled the company’s addressable market and also opened a window to potentially lock in another $300 million in revenue over the next few years.

Presentation Q3

Now, based on management’s guidance provided in Q3, it looks like TGLS would close out FY23 delivering solid top-line growth of 17%. Given a relatively strong base year, one would expect growth to slow to single-digit levels in FY24, but consensus forecasts for next year point to revenues of $925.5 millionwhich would mean another year of double-digit top-line growth.

In addition, TGLS also has a very well controlled balance sheet with a very low level of debt. The company’s cash balance, which was $50 million in the pre-pandemic era, has increased more than 2.6x, while the level of net debt has fallen to a record low. Currently at just 0.15x EBITDA at the minute and with no major maturities until the end of 2026, and with much of its short-term CAPEX commitments already covered, the company is well positioned to channel its free cash flow towards its share buybacks. For context, note that the company is currently running a $50 million buyback plan and from 9-23 18% of which.

Presentation Q3

Final Thoughts – Is TGLS a good buy right now?

Until now, we may have painted an optimistic picture of TGLS, but despite its natural strengths, we are not confident of generating excess returns at this stage.

First, note that TGLS is heavily exposed to the Florida market (91% of its business in the US) and it looks like the strong momentum in the multifamily market there is long gone and sales are down 3.4% from January. One of the key factors behind this shift was the disproportionate increase in insurance costs, which were among the highest of any US market.

Realpage

The forward valuation of TGLS is not exactly cheap at this point in time, especially in light of the medium-term earnings growth one achieves at the current multiple.

YCharts

Between FY23 and FY25, consensus expects only a 7% earnings CAGR, but the stock is priced at a double-digit P/E of nearly 11x, a 12% premium over the long-term average.

YCharts

Finally, also consider that if we were to look for suitable hackneyed opportunities in the building and construction space (to explore the mean reversion theme), it certainly doesn’t look like TGLS will turn out to be one of the best. Currently, Tecnoglass’ relative strength ratio as a function of the Invesco Building and Construction portfolio is a good 32% higher than the midpoint of its long-term range.

StockCharts

To conclude, we feel that TGLS warrants a HOLD rating at this point in time.

Sabine Royalty Trust (NYSE:SBR) has been doing very well compared to other energy funds since my September article which had a neutral/hold recommendation. As oil and gas prices have fallen more than I expected and I am not optimistic short-term energy prices, I reduce SBR for sale. Monthly distributions over the next several months may remain relatively high due to the several-month lag between production prices and announcements of monthly distribution payments, but then will likely decline as they reflect current natural gas and oil prices. Additionally, I consider SBR a sell because there are frequent adjustments to monthly statements that make it very difficult to analyze the reported numbers and estimate appropriate SBR values.

The price of SBR remained high despite lower energy prices

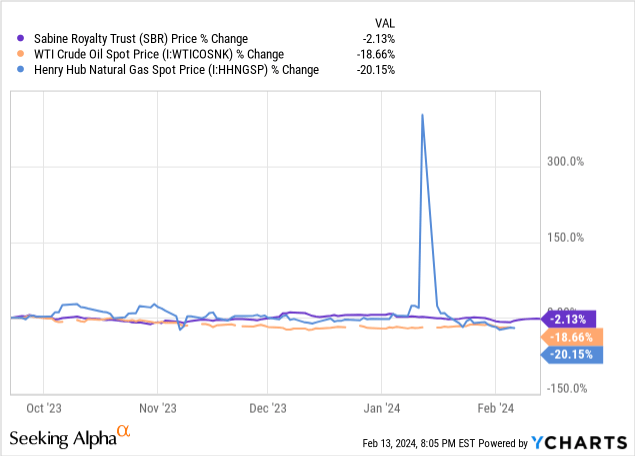

Natural gas prices have been on a roller coaster over the past five months, but the trend was lower, especially on a seasonally adjusted basis. WTI crude oil prices were also trending lower than I expected.

SBR, Henry Hub and WTI spot price changes since September Article

While oil accounted for approximately $4.36 million of them the last monthly magazine royalty revenue compared to $3.07 million for natural gas, dramatic fluctuations in natural gas prices appear to affect the SBR unit price more than modest changes in oil prices. Changes in commodity prices have a direct impact on returns because the trust cannot hedge, unlike many energy companies, which often hedge at least part of their expected future production.

I think the October 2024 Henry Hub natural gas futures (NGV2024) illustrate the dramatic decline in gas prices since I wrote my September SBR article. The October 2024 contract was trading around $4.50 at the time of publication, but this contract is now trading at $2.40. October 2024 WTI crude futures (CLV2024) fell less dramatically from around $79 to $75. The price of SBR was only down a very modest 2%.

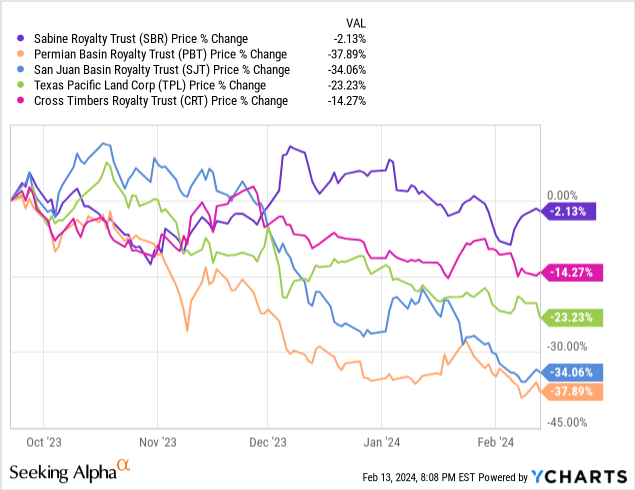

Many other energy trusts (I consider Texas Pacific Land Corp (TPL) as part of the energy trust group, although it will transform into a trust corporation in 2021) were significantly overpriced last September and the fall in energy prices accelerated their price decline. Last September, the SBR was not overpriced. However, I expect the decline in natural gas and oil prices to eventually negatively impact SBR’s unit price as monthly distributions decline later this year.

Price changes for some energy trusts since my September SBR article

I had a referral to sell on the San Juan Basin Royalty Trust (SJT) and the Permian Basin Royalty Trust (PBT) as of Q2 2023, but if I were to write an updated article today, I would now consider both SJT and PBT to be holds. While both are not just royalty funds (they also have working interests), many investors look at them in comparison to SBR.

Outlook for oil and natural gas prices

Energy prices continue to be influenced by geopolitical events. For two years it was the war in Ukraine and more recently it was problems with shipping in the Red Sea. If President Biden exerts pressure to negotiate a settlement of the Ukraine war, he could attempt a “victory lap” for his foreign policy, which could affect the November election. The settlement could have the psychological impact of lowering oil and gas prices with expectations of increased supplies coming to the market from Russia. The increase in actual deliveries (if any) is uncertain.

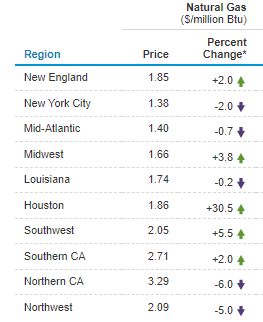

US Energy Information Administration – EIA – predicted average spot natural gas prices will rise to $2.65 in 2024 and $2.94 in 2025 from $2.54 in 2023. Their forecast is based in part on the completion of three LNG export facilities in 2024 and 2025. Biden’s decision temporarily “suspend the pending decision on exports of liquefied natural gas (LNG) to non-FTA countries until the Department of Energy can update the underlying analysis for the permit” could have a long-term impact on natural gas prices unless Trump reverses it (if elected.)

Natural gas February 12 Spot prices by region

www.eia.gov

The EIA’s projected increase in natural gas storage will most likely cap any sustained spikes in gas prices caused by weather or political events. You can still see very short-term spikes, such as what happened in January caused by very cold temperatures, but market supply will adjust fairly quickly as storage space declines.

Natural gas storage and deviation from the mean

eia.gov

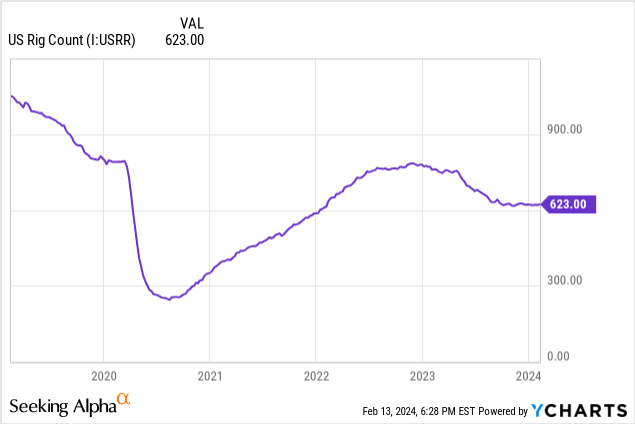

Some energy bulls may argue that since the weekly U.S. rig count has fallen from more than 780 in December 2022 to the current 623, prices will rise because supply will eventually fall. I’m not a big fan of looking at the total number of rigs when predicting future oil and gas supplies, as there are many variables behind that total. For example, actual production from a drilled well varies by watershed. The time required to complete the well is another critical factor. If one rig crew drills much faster than historical averages, the number of wells over time will be higher.

I’m not sure if their accounting problems are due to the very large number of actual operators compared to other energy trusts who may only have one or two operators, but there are frequent adjustments in their monthly reports based on updated numbers. For example, their December 2023 Press Release the monthly distribution includes oil production in September, but the number was positively impacted by 103,000 barrels of oil from 14 new wells for the period from May 2022 to August 2023. The 103,000 brought the monthly amount to 189,898 barrels. In other words, those investors who held SBR during this long period got “short changed” on their monthly distributions because the oil revenue from those 14 wells was not included in the returns that determine the monthly distribution. However, SBR holders on the record date of December 15, 2023 received a total “bingo” distribution of $1.143090 per unit per month.

Comparing monthly production numbers also complicates the timing of actual royalty income. As stated in their latest press release dated February 5th: “Due to the timing of the end of January, approximately $619,084 of revenue received will be booked in the following month of February, in addition to the normal cash revenue received during February.” The 3rd of November the press release was even worse: “Due to the timing of the end of the month of October, approximately $10,484,301 of received revenue will be accounted for in the following month of November, in addition to normal revenue during November.” How much of that nearly $10.5 million comes from oil and how much from gas? How much production and average cost resulted in $10.5 million? The reality is that much of that $10.5 million comes from the 103,000-barrel adjustment reported in December, but investors were confused by the announcement in November.

I mentioned the reporting issue in my previous SBR article, but it seems to be getting worse, or maybe the maintainer is getting more diligent about reporting bugs. According to a statement contained in their January 5th press release: “Early in the fourth quarter, Sabine Royalty Trust hired a new revenue processor.” Their accounting problems could have a negative impact on rational investment decisions. If investors decide to sell their SBR units based on disappointing results contained in a monthly press release, but then a few months later the original news is revised upwards, those investors will most likely feel very frustrated.

Sabine Royalty Trust Valuation

Many investors look only at the distribution yield when valuing SBRs. In my September article, I used an estimated gas price of $1.89 and an oil price of $89 to estimate an average monthly distribution of $0.40 or an annual distribution of $4.80 per unit. I am slightly lowering my gas price estimate and lowering my oil price estimate to $75. My new estimated average monthly distribution is now $0.33 or $3.96 per year starting at the end of Q2 2024 and beyond. Using SBR’s most recent price of $62.78, the implied yield is 6.3% with an annual distribution of $3.96. The 6.3% yield is only 165 basis points higher than the current 4.65% yield on 2-year US Treasuries. This spread is not high enough due to the high risk associated with the trust, which is directly affected by extremely volatile commodity prices.

Conclusion

The Sabine Royalty Trust has the advantage of not being dependent on just one or two energy companies for royalty payments. However, accounting/reporting also seems to cause this diversification problems. PUSH there are frequent monthly adjustments that make it very difficult to properly analyze their monthly reported numbers. I see this as a major negative for SBR investors.

Dramatic weather and geopolitical events could affect the price of oil and natural gas, but assuming significant events occur, I expect energy prices to decline slightly and remain relatively low through the remainder of 2024. Given this forecast, I estimate that monthly distributions later this year they will average $0.33. The resulting yield of 6.3% is too low to justify holding SBR compared to other income-producing investments. I am now rating the SBR as a sale.

Although it is not the biggest player in alcoholic beverages, Molson Coors Beverage Company (NYSE:TAP) is a real giant in this market. The company’s market cap as of date is $13.39 billion this writing and owns a wide variety of leading brands such as Coors Light, Miller Lite, Molson Canadian, Miller High Life, Vizzy Hard Seltzer and more. Even with such a packed portfolio of brands, the company faces tough competition from other players in this field. Therefore, it is imperative that investors continue to monitor financial results as they become available. How a company performs from quarter to quarter shows over time how well it is meeting expectations.

Looking at last quarterwhich is the last quarter fiscal year 2023 that management just reported On February 13, the company delivered a mixed performance. Sales were higher than expected. Adjusted earnings also did well. But GAAP earnings fell short of forecasts.

Ignoring analysts’ expectations for a moment, the overall trend in business seems to be positive. Sales grow and cash flow usually follows. Additionally, the company’s shares are trading at a discount compared to similar large players. All of these factors, combined, lead me to believe that this is a solid “buy” candidate at this time.

Keep up with the company

Before we get to the fundamental results announced on February 13th, it might be helpful to dive a bit into the overall operations of Molson Coors Beverage Company. As I have already stated, the company operates mainly as a liquor store. Its oldest predecessor, Molson, dates back to 1786, making it one of the oldest companies in the Western world still in existence.

From its humble beginnings, the business has grown into an international player in the beverage market. However, it should come as no surprise to investors that the bulk of its business comes from North America. In fact, according to management, the company is the oldest beer company and the second largest brewer by volume on the continent. Overall, it claims to have roughly a 20% market share in the region.

The company also operates elsewhere. These international operations are conducted through the EMEA & APAC segment, which includes its primary brands, as well as licensed brands, in a number of countries across Europe, the Middle East, Africa and the Asia-Pacific region. The company also claims to be the second largest brewer by volume in the European countries in which it operates, with a total market share of 18%.

Of course, Molson Coors Beverage Company sells more than just alcoholic beverages. Some of its soft drinks include those that contain cannabis and are sold in Canada through a joint venture it has with HEXO Corp. The company also boasts deals that allow it to cook, pack and ship products on behalf of other smaller players. such as The Yuengling Company, Pabst Brewing Company and Labatt USA Operating Co.

By SEC EDGAR Data

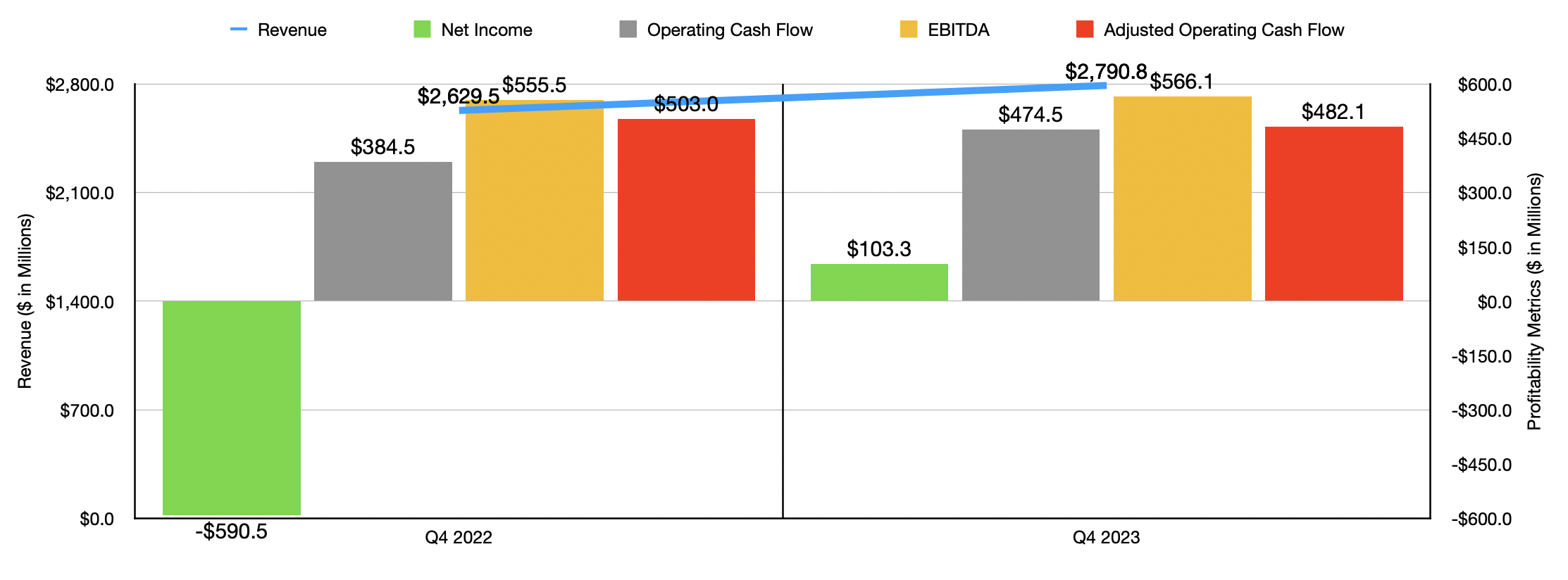

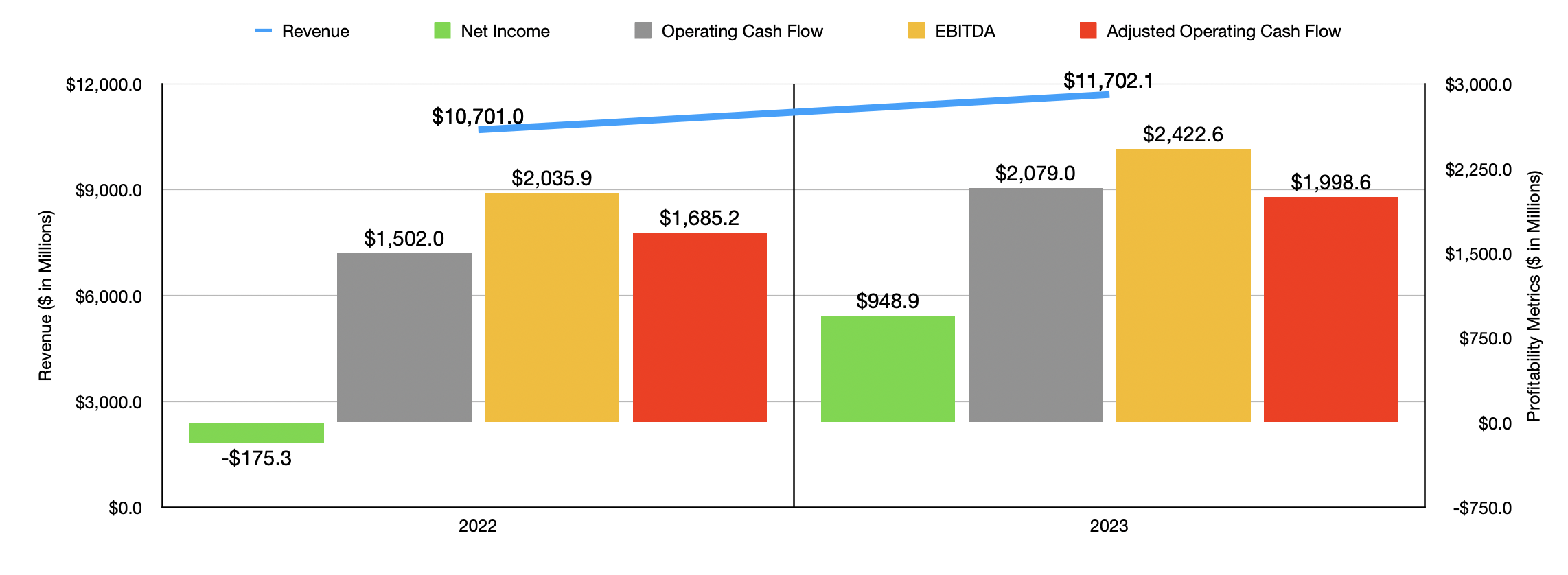

Basically, the image of the company has been rising recently. As an example, just look at the data for the last quarter of fiscal year 2023. Revenues at that time reached $2.79 billion. In addition to coming in 6.1% higher than the $2.63 billion the firm generated in the same period a year ago, it was also $10 million higher than analysts. predicted per quarter.

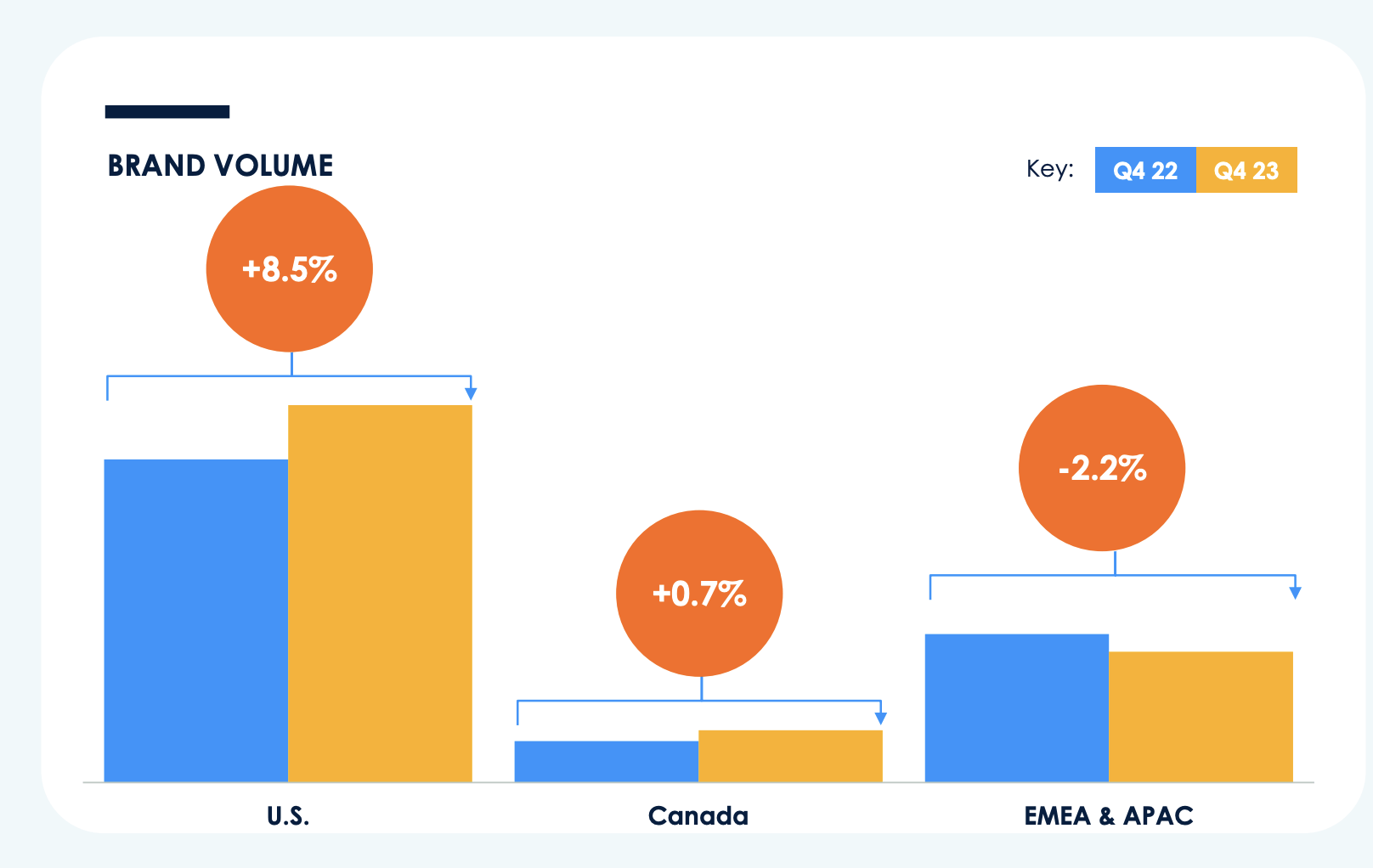

Part of the increase in sales was due to foreign currency fluctuations. Without them, sales would have increased by about 5%. The company’s ability to raise prices and changes in product mix helped increase sales by 4.2% year over year. However, the company also benefited slightly from it sent higher volumes during the quarter. Financial brand volumes in the Americas, for example, jumped 4.3% year-over-year, with the Americas leading the way with a 6.7% increase. The company’s core brands were responsible for an 8.5% increase in brand volume in the US market.

Molson Coors Beverage Company

Unfortunately, North America was not representative of the wider world. The EMEA and APAC segment actually saw brand volume decline by 2.2% year-on-year due to the negative impact of inflation in places like Central and Eastern Europe. Softness in the UK space was also problematic. But there was a certain weakness in North America as well. In Latin America specifically, weak demand and overall economic conditions reduced volumes by 5%. And even in Canada, volume was up just 0.7%. And according to management, it was only because of the strength of the premium offers that the company has.

The increase in sales led to an improvement in the economic result. The company went from generating a net loss of $590.5 million to a profit of $103.3 million. This moved the company’s earnings per share from a negative $2.73 to a positive $0.48. As visible as the move was, earnings fell short of the $1.13 per share analysts had predicted. But on an adjusted basis of $1.19 per share the company reported, it beat estimates by $0.07 per share.

Other profitability metrics largely followed suit. Operating cash flow increased from $384.5 million to $474.5 million. Unfortunately, it’s worth noting that after adjusting for changes in working capital, cash flow fell slightly from $503 million to $482.1 million. But EBITDA helped offset that, rising from $555.5 million to $566.1 million.

By SEC EDGAR Data

As you can see in the chart above, results for fiscal year 2023 as a whole were better than results for 2022. Without exception. Management was clearly satisfied and seemed optimistic about the future as it took care of directly rewarding shareholders. The annual dividend paid by the company during 2023 was 8% higher than in 2022. The company also took care of share repurchases worth $205.8 million for the year. That stacked up nicely compared to the $51.5 million worth of stock bought back in 2022.

Most likely, share buybacks will continue. I say this because in October 2023, the company announced a new, larger buyback program that would allow the company to buy up to $2 billion worth of its units over a five-year window. The $150 million in share buybacks the company made last year came from this program, with all of those purchases spread out between November and December. So if anything, business is just getting started.

Of course, the company does not forget its own financial health either. Management decided to reduce net debt by $607.3 million last year. This brings total net debt down to $5.36 billion.

Molson Coors Beverage Company

Looking to fiscal 2024, management believes that sales will grow at a low single-digit rate on a constant currency basis. While not impressive, it’s better than a drop in sales. Underlying EPS growth is trending toward the mid-single digit range. If we assume that translates into a 5% year-over-year growth rate, and if we ignore the prospect of share buybacks, we’d be looking at net earnings for the year of $996.3 million.

Following further company guidance, I was able to obtain rough approximations of operating cash flow and EBITDA. According to my estimates, it should be $1.95 billion and $2.22 billion.

By SEC EDGAR Data

Using these results I was then able to value the business as shown in the chart above. The stock actually looks quite attractive, especially from a cash flow perspective. To follow up on this, I created the table below. In it, you can see how the stock stacks up against four similar companies. Interestingly, the units were cheaper than all four companies in all three different scenarios. So in addition to being attractively priced on an absolute basis, the units are attractively priced relative to other players.

All I can say at this point is that I believe Molson Coors Beverage Company is doing a good job. While it’s disappointing to see Q4 earnings fall short of expectations, and it would be nice to see adjusted operating cash flow increase year-over-year, the overall picture for the company is positive. If my estimates are correct, cash flows will be slightly lower this year than they were in 2023. But given how cheap the stock is, both absolutely and relative to peers, Molson Coors Beverage Company’s valuation is solid “ buy”. it seems digestible.

Editor’s note: This article discusses one or more securities that are not traded on a major U.S. stock exchange. Please be aware of the risks associated with these shares.

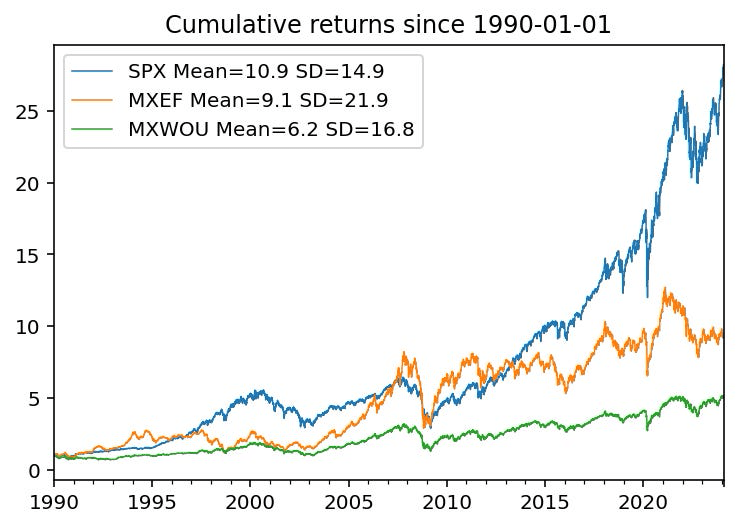

Emerging market and non-U.S. developed market stocks have underperformed their U.S. counterparts over the past few decades. There are several possible explanations for this lack of performance. First, it is possible that the risk premium for holding US stocks is greater than the risk premiums associated with holding international shares. Since US stocks are also significantly less volatile than international stocks, this is unlikely to be the reason.

The average is the annual average return of each market for US-based investors. SD is the annualized volatility of stock returns. Key: SPX = S&P 500; MXEF = EM shares; MXWOU = Global Equities Outside the US (Bloomberg, QuantStreet)

Another reason may be that capital is not perfectly mobile across countries (ie, foreign investors are either unable or unwilling to own “enough” US stocks), and because of unique local conditions (ie, a highly dependent and productive corporate sector). ), US stocks they have structurally higher expected returns than stocks from other countries, despite having lower risk. That’s not the focus of my article, but it seems like a plausible explanation.

Third, it is possible that investors are too bullish about the prospects for the US stock market. It’s hard to disprove, but this looseness has been around for decades, and a few US stock market crashes (’99-’01, ’08-’09, and 2020, for example) weren’t enough to reverse the effect. .

Finally, it may be that relative investment conditions have changed over time to favor the US over other global equity markets, and that investors are slow to respond to this information (consistent with the macro momentum effect documented AQR and other). While there may be other potential explanations, in this article I analyze this last spread – the relative attractiveness of US markets.

Impact on capital flows

In his 2015 book Unraveling the Emerging Markets EnigmaAndrew Karolyi analyzes the effects of six country-level risk indicators on the extent to which US residents over- or underinvest in foreign stock markets. In his work, allocations of US residents to foreign stock markets, measured in US dollars, come from US Treasury International Capital Database as of the end of 2012. Overinvestment or underinvestment is measured relative to a country’s stock market capitalization divided by the sum of all countries’ stock market capitalizations as of the end of 2012. The six indicators Karolyi uses to analyze a country’s level of risk are:

market capacity limitations,

operational inefficiency,

restrictions on foreign investment,

corporate opacity,

limitation of legal protection and

political instability.

All these measures are explained in detail in the book. The convention is that higher levels of variables mean better results (eg, more openness and less restriction; see pp. 11-12 of the book). Table 10.2 of Karolyi (2015) shows that a one standard deviation increase in the mean of these six indicators (meaning less restriction, less opacity and more legal protection – presumably also measured in 2012 – see p. 183) is associated with 1.24 % increase in the relative allocation of capital investment of US residents to that country. Compared to typical over- or under-allocation, this is a very large effect. A one standard deviation improvement in legal protection and a one standard deviation decrease in political instability are associated with an increased relative country allocation of 0.57% and 0.91%, respectively. All three effects are statistically significant and economically large.

Table 10.4 of Karolyi (2015) makes a similar point when looking at country-level equity allocations of global institutional investors. Karolyi’s (2005) conclusion is that investor capital tends to flow to countries that open up to foreign investors and tend toward political stability and the rule of law. Aggregating these effects to the stock index level, e.g., all countries or only EM countries, suggests that a deterioration in the average index score on these dimensions should be associated with investor outflows and likely poor index returns for the duration of the outflow episode. Since capital flows are slow, such underperformance can persist for a long time.

CATO Freedom Index

The CATO Institute publishes an annual study called Human Freedom Indexwhich analyzes economic and personal freedom at the country level in 86 dimensions, including:

legal state,

legal system and property rights,

and an aggregate measure of freedom called the human freedom index.

Although I do not have access to recent values of Karolyi’s (2015) six risk measures, in the following I assume that CATO’s human freedom, rule of law, and legal protection scores are good proxies for Karolyi’s mean of the six indicators, political instability, and limitation of legal protection measures.

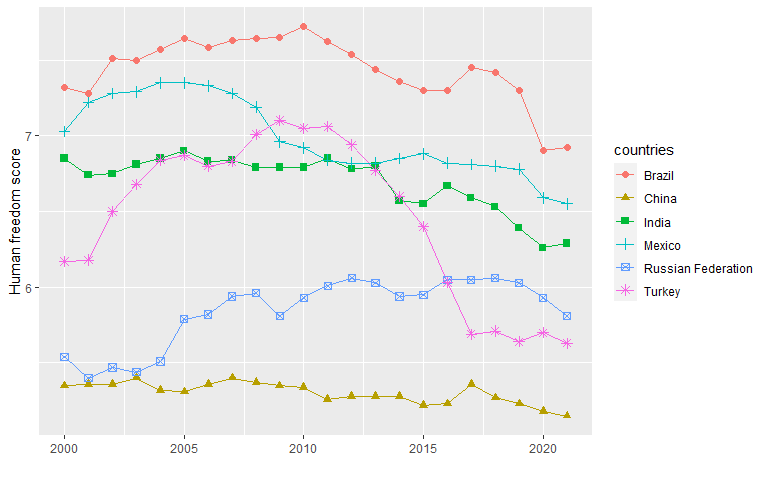

The following chart shows the Human Freedom Index for some prominent countries that are currently in the EM index, as well as Russia, although it is no longer part of the index. The main finding is that many large emerging market economies saw significant improvements in their human freedom scores from 2000 to 2010—a time period closely related to the emerging market stock market outperformance seen in the chart above—only to this trend has begun to reverse. in the last decade. This deterioration has been much discussed in the financial press, with some arguing that some EM markets such as China could become “non-investable.”

CATO Institute, QuantStreet

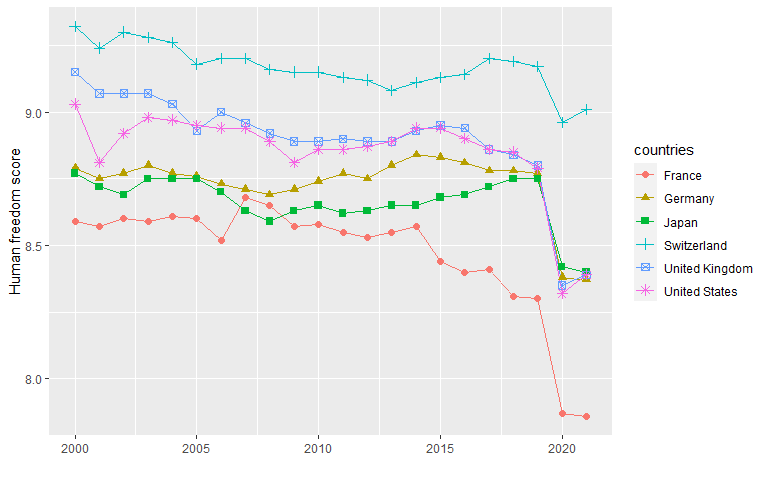

Looking at major advanced market economies, the biggest shake-up to freedom in the last two decades has been caused by COVID-19. As the CATO Human Freedom Index 2023 report states: “A key question in the coming years is whether governments will fully lift the restrictions on freedom related to COVID as the pandemic eases, or whether some will continue to apply the additional control and purchasing power they appropriated during the pandemic.“Several countries such as Switzerland, the UK and the US have already shown that they have reversed some pandemic-era restrictions, although others such as France, Germany and Japan have yet to do so.

CATO Institute, QuantStreet

According to Karolyi (2015), these trends in developed and emerging market economies do not bode well for international investors’ interest in global stock markets.

Aggregate ETF-level openness

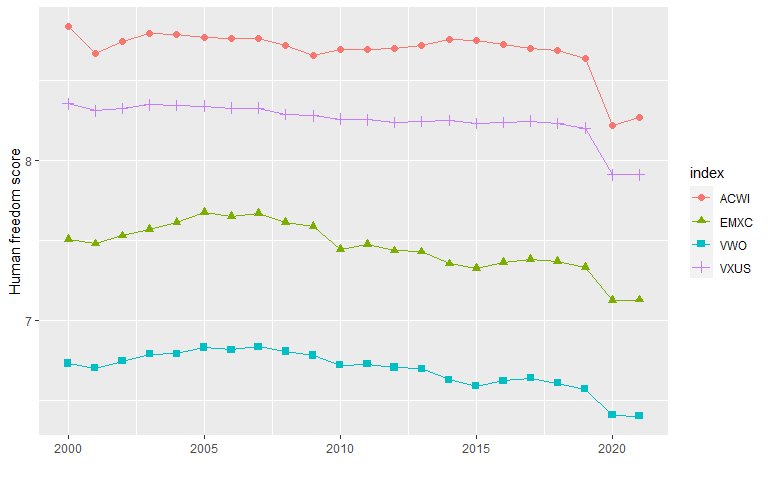

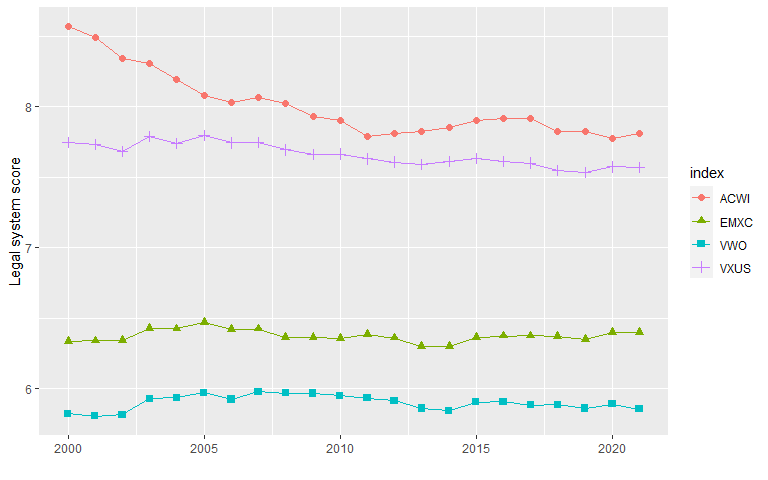

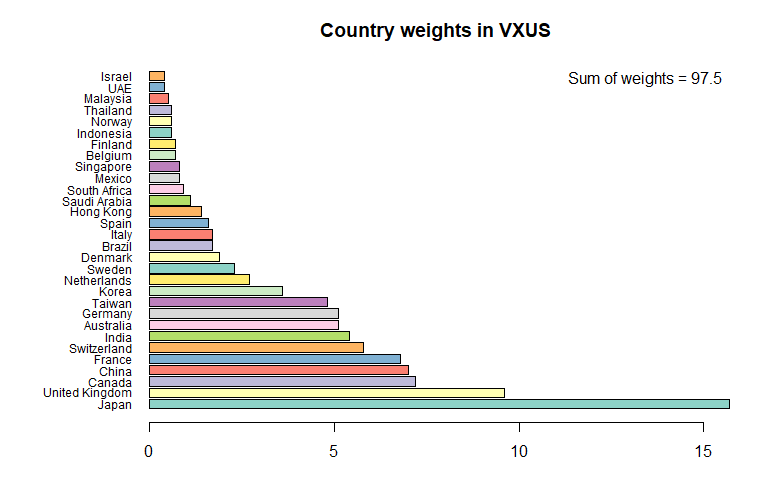

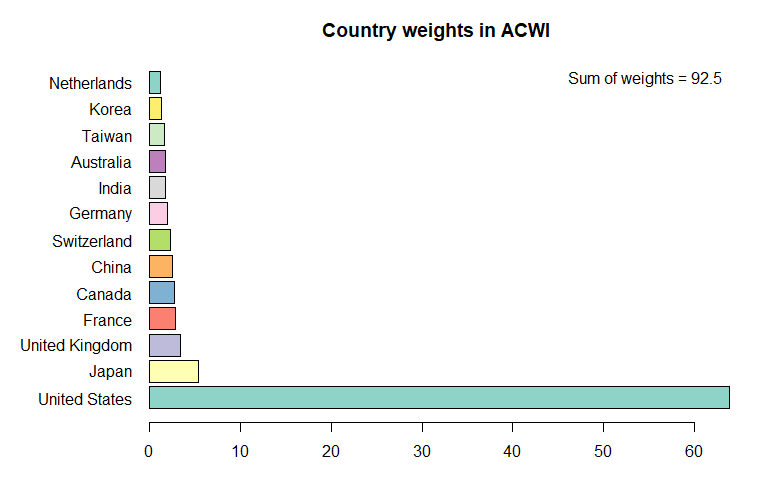

To understand how these trends play out in the world’s major stock market indices, the next set of charts aggregates country-level Human Freedom Index scores into ETF-level measures using each country’s market capitalization weights in the ETF (see the charts at the end of this article for ETF country weights ). ACWI, an ETF tracking the MSCI All Country World Index with a roughly 64% allocation to the US equity market, has the highest aggregate human freedom score, followed by VXUS, Vanguard’s global ex-US equity ETF. The main difference between the two is the absence of a US allocation in the VXUS, indicating that the US has a higher average human freedom score compared to the value-weighted scores of countries in the VXUS. Both ACWI and VXUS freedom scores declined in 2020 due to COVID-19 restrictions, although ACWI scores have begun to rebound.

CATO Institute, QuantStreet

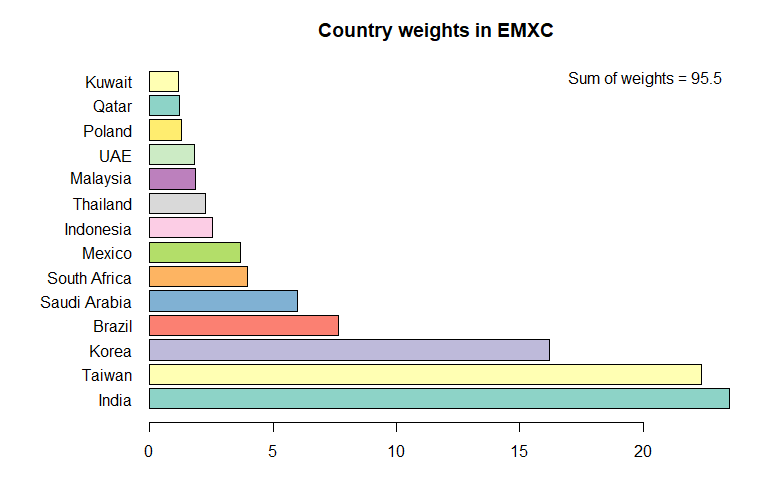

When it comes to EM, the VWO ETF (Vanguard’s EM fund) has the lowest overall human freedom score. VWO’s freedom score has been declining since its peak in 2007, coinciding exactly with the end of EM outperformance in the mid-years. The EM ex-China ETF, whose largest country weightings are India, Taiwan, Korea, Brazil and Saudi Arabia, has a higher human freedom score than VWO, but is still well below the heavier weighting VXUS and ACWI ETFs. developed markets.

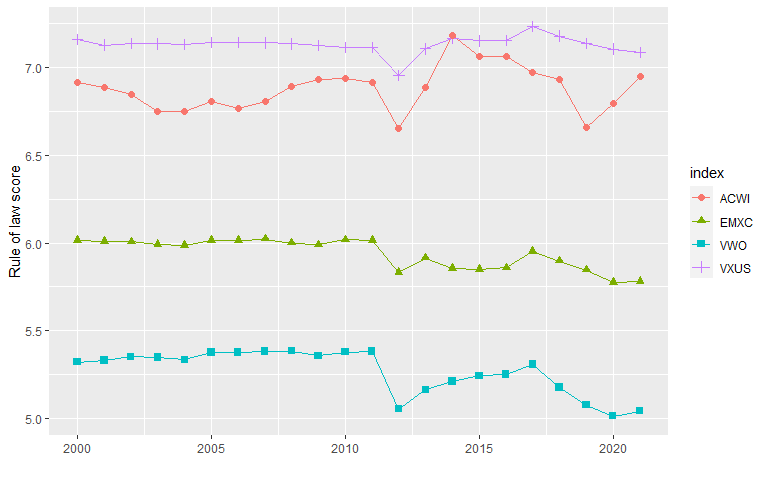

As the following two graphs show, the picture when looking at aggregate measures of legal protection and rule of law is largely similar. Developed markets are well ahead of their emerging market counterparts, and emerging markets from China are outperforming the overall China-weighted emerging market index.

CATO Institute, QuantStreet

The trends in the assessment of legal protection and the rule of law on EM are negative, which reinforces the deduction from the main measure of human freedom.

CATO Institute, QuantStreet

Investor withdrawals

One of the puzzling market phenomena over the past few decades has been the underperformance of global stock markets relative to the US. While there are many potential reasons for this underperformance – some have to do with differences in productivity and innovation at the country level, which I don’t understand. discuss in this article – one possible explanation is that non-US stock markets, with a few notable exceptions, are generally less open and have weaker legal protections and rule of law measures than the US Karolyi (2015) and other academic work. argued that such openness and legal predictability are important for attracting investor capital and promoting economic growth. The trend in these measures, especially in emerging markets, is not pointing in the right direction, suggesting that future returns may continue to favor US markets as they have for the past several decades.

Country weights in various ETFs

The following few charts show country market capitalization weights in various international and global ETFs. These weights are used to aggregate CATO Human Freedom Index scores into ETF-level measures.

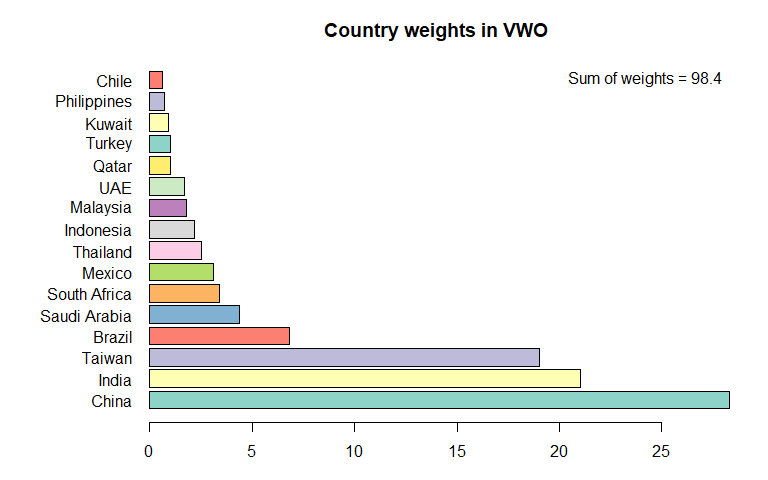

The following chart shows the weights in the EM index.

Vanguard, QuantStreet

The following chart shows the weights in the EM ex-China index.

iShares, QuantStreet

The following chart shows the weights in a global, ex-US stock index.

Vanguard, QuantStreet

The following chart shows the weights in a global stock index that includes the US

You don’t see liquidations in the closed-end fund (CEF) space very often, but they do happen from time to time. Liquidations are ideal arbitrage opportunities, especially when CEFs are trading at a discount to net asset value. It here is this case MFS Special Value Trust (MFV), which we discussed earlier here. In our original news article, we found nothing particularly attractive about this CEF. The fund is very small (roughly $31 million at Seeking Alpha) and has poor historical performance that has failed to impress.

The fund manager seems to have come to a similar conclusion notification on 13 February 2024 that the CEF is to be liquidated. In this article, we will examine this company stock in light of the fund structure and derive an opinion on how the retail investor should take advantage of this rare development.

CEFs don’t liquidate often, but MFV is about to

On February 13, 2024, the fund manager made a surprising decision to close the CEF through liquidation:

BOSTON–((BUSINESS WIRE))–MFS Investment Management® (“MFS®”) announced that at today’s meeting, the Board of Directors of the MFS® Special Value Trust (the “Fund”) (NYSE: MFV), a closed management investment company, approved the liquidation and liquidation plan of the fund (hereinafter referred to as “liquidation”). The liquidation is currently expected to be completed on or about April 29, 2024.

After the effective date of the plan of liquidation (approximately April 10, 2024), the fund will commence an orderly liquidation of its assets, determine and pay or set aside in cash or cash equivalents an amount at least equal to all known or reasonably ascertainable liabilities and obligations of the fund and make one or more liquidation payments jointly shareholders of the fund. The Fund may also begin liquidating certain holdings prior to the plan’s effective date. The Fund has set the termination of operations on April 10, 2024 as the effective date for determining the Fund’s common shareholders entitled to receive liquidation payments

We call this decision surprising because management teams often do not liquidate CEFs because of the fee income they generate and the ability to sell the structure, as we saw with VCIF (covered herewith CEF now called CCIF after the sale).

The fund’s asset management team appears to have considered other alternatives but ultimately settled on liquidation. We think it speaks well of the management team because it’s doing something favorable for shareholders. The smaller a CEF, especially one that allocates to fixed income, the more difficult it is to get positions in certain names (kindly remember some names in the fixed income business with minimum sizes, sometimes $500,000 or $1 million).

Possibility of liquidation arbitration

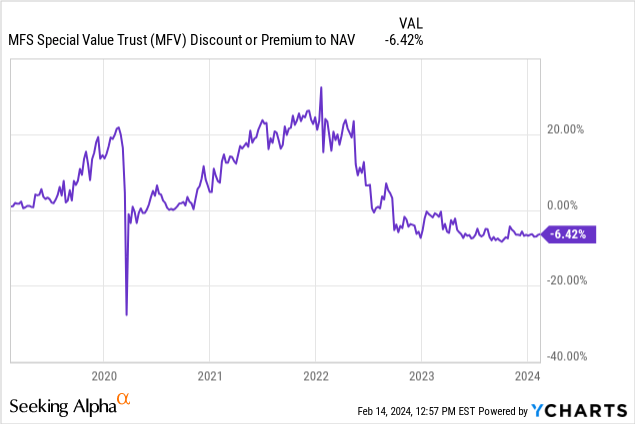

The arbitrage opportunity is quite simple for CEF. If a CEF trades at a discount to NAV and a liquidation occurs, the retail investor can cash out the difference between the fund’s NAV and market value. MFV is currently trading at a significant discount to net asset value:

CEF is trading at a -6.4% discount to NAV, a discount that will move to NAV in the coming days as market prices are liquidated.

With the liquidation date around the corner, expect the market to close most of the arbitrage gap this week. Market participants now only attribute the full value of the collateral, given the close conversion to cash.

Risk factors for the arbitrage game

The arbitrage opportunity here relates to the market fully pricing the CEF collateral. As an investor, you will still bear the market risk associated with holding equities and fixed income in the fund. However, considering the short time window, the market risk is slightly reduced. If the market remains at current levels, expect to realize a +6.4% gain from the disappearance of the discount to NAV plus any dividend income accumulated by the fund.

On the stock side, the fund has a financial and insurance slant, with its top 10 holdings including JPMorgan Chase (JPM) and Cigna (WHOSE). This is a robust allocation as large companies are less exposed to potential volatility stemming from a renewed regional banking crisis. In fact, the entire fund is concentrated in big names in terms of stocks. On the fixed income side, the portfolio is mostly high yielding and therefore subject to credit spreads until liquidation.

Please note that the collateral is non-maturity, which means that the fixed interest instruments in this portfolio have maturities well beyond the liquidation date of the fund.

Conclusion

MFS Special Value Trust is a multi-asset CEF that we covered earlier. The vehicle announced its liquidation on February 13, offering retail investors a rare CEF liquidation arbitrage opportunity. The fund was trading at a -6.4% discount to its net asset value at the close of business on February 13, giving investors the opportunity to buy shares at a deep discount, with full value on April 29, 2024. This arbitrage opportunity is very attractive due to the quick turnover, but it is not without risks as the investor would still be subject to market fluctuations of the underlying collateral.

Editor’s note: This article covers one or more microdroplet stocks. Please be aware of the risks associated with these shares.

The Seeking Alpha transcription team is responsible for the development of all our transcription related projects. We currently publish thousands of quarterly earnings calls quarter after quarter on our site and continue to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new developments related to transcripts. Thanks, SA Transcripts Team